Introduction: Your Guide to Post-Service Benefits

Transitioning from military to civilian life is a significant step. It comes with unique opportunities and challenges. Fortunately, you have earned a wealth of benefits designed to support this new chapter.

This guide is your roadmap to understanding and accessing these vital resources. We will explore the comprehensive support systems available to you. These include programs from the Department of Veterans Affairs (VA) and various other organizations.

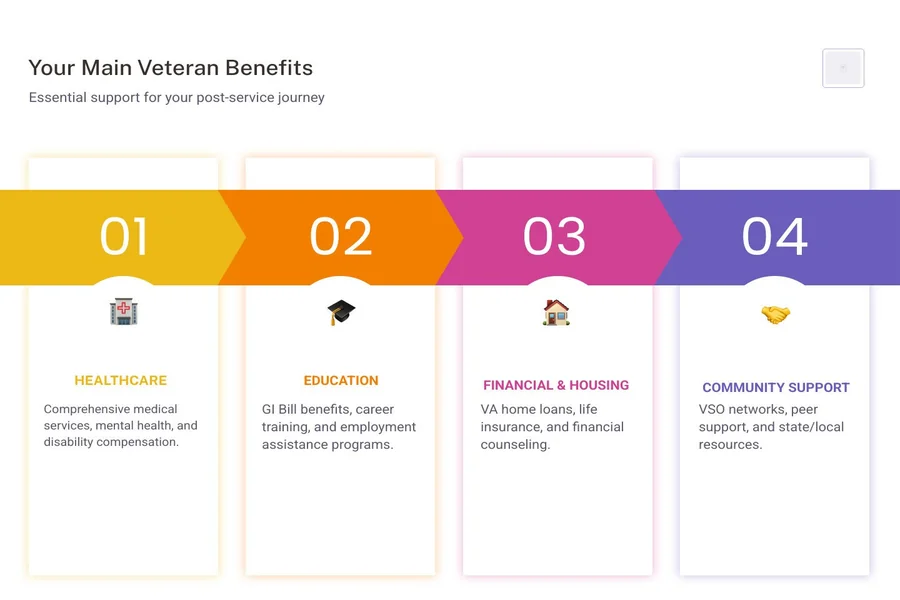

Our goal is to help you confidently steer your post-service journey. We will cover key areas such as healthcare, education, financial assistance, and community connections. Look for our infographic below for a quick overview of these main benefit categories.

Healthcare and Wellness Support

One of the most critical aspects of post-service life is ensuring access to quality healthcare and maintaining overall wellness. The VA Health Care system is a comprehensive network designed to meet the unique needs of veterans, offering a wide array of services from routine check-ups to specialized treatments.

Eligibility for VA healthcare is based on various factors, including your service history, income level, and whether you have a service-connected disability. The enrollment process typically involves submitting an application, after which the VA will determine your priority group. This priority group dictates the level of benefits you receive and how quickly you can access care.

Beyond physical health, the VA places a strong emphasis on mental health services. Vet Centers, for instance, offer free and confidential counseling to veterans, service members, and their families, addressing issues such as PTSD, grief, and readjustment challenges. These centers provide a safe space for veterans to connect with peers and receive professional support.

For those whose service has resulted in illness or injury, disability compensation is another crucial benefit. This tax-free monetary benefit is paid to veterans with disabilities that are a result of a disease or injury incurred or aggravated during active military service. Understanding how to apply for and manage these benefits is vital for long-term financial stability and access to care.

Navigating Healthcare: Key Veteran Resources

The VA medical benefits package is extensive, covering a wide range of services. This includes preventive care, primary care, specialty care, and even emergency services. For women veterans, dedicated Women Veterans Health Care programs ensure gender-specific services are provided with sensitivity and expertise. Similarly, Geriatrics and Extended Care programs cater to the needs of older veterans, offering nursing home care, home health services, and palliative care.

Specialized care programs address unique conditions such as traumatic brain injury (TBI), spinal cord injury, and prosthetics. Mental health support is robust, with various treatment modalities available, including individual and group therapy, medication management, and substance use disorder treatment. The VA also operates a confidential Veterans Crisis Line, available 24/7, providing immediate support for veterans in emotional distress or at risk of suicide.

Filing for Disability Compensation

If you believe your current health conditions are related to your military service, filing for service-connected disability compensation is a crucial step. The VA claim process can seem complex, but with proper preparation, it is manageable. You will need to gather evidence, which typically includes your service medical records, private medical records, and potentially lay statements from yourself or others who can attest to your condition and its impact.

The VA assigns disability ratings, expressed as percentages, which reflect the severity of your service-connected condition and determine the amount of compensation you receive. Working with a Veterans Service Officer (VSO) can significantly streamline this process. VSOs are accredited professionals who can help you understand your benefits, gather necessary documentation, and file your claim accurately. Their services are typically free and invaluable for navigating the bureaucratic landscape.

Education and Career Advancement

The skills, discipline, and leadership qualities developed during military service are highly transferable to civilian careers. However, further education or specialized training can often bridge the gap to new opportunities. The VA offers several robust programs to support your educational and career goals.

The Post-9/11 GI Bill is perhaps the most well-known, providing financial support for tuition, housing, and books for eligible veterans pursuing higher education or vocational training. For those who served prior to September 11, 2001, the Montgomery GI Bill offers similar benefits. These programs are designed to help you achieve your academic aspirations without the burden of significant debt.

Beyond traditional schooling, Veteran Readiness and Employment (VR&E), formerly known as Vocational Rehabilitation and Employment, assists veterans with service-connected disabilities in preparing for, obtaining, and maintaining suitable employment. This can include vocational counseling, job search assistance, and even tuition for specific training programs. Additionally, the VA supports apprenticeships and on-the-job training, allowing veterans to learn a trade or skill while earning a wage.

Utilizing Your GI Bill Benefits

Choosing between the Post-9/11 GI Bill and the Montgomery GI Bill often depends on your service dates and personal circumstances. It’s important to compare the programs to see which offers the best benefits for your specific educational path. The Post-9/11 GI Bill, for example, offers a Monthly Housing Allowance (MHA) and a stipend for books and supplies, in addition to tuition coverage.

For service members looking to share their benefits, the Transfer of Entitlement allows eligible individuals to transfer unused Post-9/11 GI Bill benefits to their spouse or dependent children. The Yellow Ribbon Program further improves the Post-9/11 GI Bill by helping cover tuition costs that exceed the VA’s maximum contribution at private or out-of-state public schools.

Here are the general steps to apply for education benefits:

- Confirm Eligibility: Review your service record to ensure you meet the minimum requirements for your chosen GI Bill program.

- Gather Documents: Collect your DD214 (Certificate of Release or Discharge from Active Duty) and any other relevant service records.

- Apply Online: Complete and submit VA Form 22-1990, “Application for VA Education Benefits,” through the VA.gov website.

- Select a Program: Choose an accredited educational institution or training program.

- Submit Enrollment: Provide your Certificate of Eligibility (COE) to your school’s certifying official, who will then submit your enrollment information to the VA.

Career Transition and Employment Services

The transition from military to civilian employment can be challenging, but numerous resources are available to help. VA employment services offer career counseling, job placement assistance, and connections to employers who value veteran talent. The Department of Labor’s Veterans’ Employment and Training Service (DOL VETS) also provides extensive support, including job search tools, training programs, and employment rights information.

Building a strong civilian resume that effectively translates military experience into marketable skills is crucial. Workshops and online tools are available to help you with resume building and honing your interview skills. Veterans also benefit from federal hiring preference, which gives them an advantage in applying for federal jobs. For those with an entrepreneurial spirit, programs and resources exist to support veterans in starting and growing their own businesses.

Essential Financial and Housing Veteran Resources

Financial stability is a cornerstone of a successful post-service life. The VA offers a variety of financial programs designed to help veterans manage their money, protect their families, and achieve significant life goals like homeownership.

Financial counseling and debt management services are available to help veterans steer financial challenges, create budgets, and address debt. Life insurance options, such as Servicemembers’ Group Life Insurance (SGLI) and Veterans’ Group Life Insurance (VGLI), provide peace of mind for your loved ones.

Among the most impactful benefits, however, are the VA home loan programs. These benefits have empowered millions of veterans to achieve the dream of homeownership, often with terms more favorable than conventional mortgages.

Securing a Home with a VA Loan

The VA home loan program is a cornerstone benefit for eligible service members, veterans, and surviving spouses. Unlike traditional mortgages, VA loans are not issued by the VA itself but are guaranteed by the VA, reducing the risk for private lenders. This guarantee allows lenders to offer highly attractive terms, making homeownership more accessible.

A primary benefit of the VA loan is the absence of a down payment requirementfor most eligible borrowers. This is a significant advantage, as nearly 90% of all VA-backed home loans are made without a down payment, according to recent statistics. Furthermore, VA loans do not require Private Mortgage Insurance (PMI)or Mortgage Insurance Premiums (MIP), which can save borrowers hundreds of dollars each month compared to conventional or FHA loans. This feature alone makes VA loans incredibly competitive.

To qualify for a VA loan, the first step is to establish your eligibility and obtain a Certificate of Eligibility (COE). This document confirms to lenders that you meet the VA’s service requirements. Veterans typically need their DD Form 214 (Certificate of Release or Discharge from Active Duty) to get a COE, while active-duty personnel usually need a statement of service signed by their commander. Surviving spouses also have a specific process for applying for a COE. In most cases, a lender can obtain a Veteran buyer’s COE in just one day, a significant improvement in efficiency.

Basic eligibility requirements generally include specific lengths of service during wartime or peacetime, or six years in the National Guard or Reserves. Even if you don’t meet the minimum service requirements, you may still be eligible if you were discharged due to a service-connected disability or certain other qualifying exceptions. For more in-depth information on eligibility, the VA’s official website provides comprehensive details.

Comparing VA loans to conventional home loans highlights several benefits. Beyond no down payment and no PMI, VA loans often come with competitively low interest rates due to the government guarantee. They also have more flexible credit score requirements, though lenders will have their own minimums. The VA also limits the closing costs you can be charged, further reducing the financial burden. Since 1944, the VA has helped over 25 million military men and women purchase homes, demonstrating the profound impact of this program. For more in-depth information, explore these VA loan veteran resources.

Understanding Different VA Loan Options

The VA loan benefit isn’t a one-size-fits-all solution; it encompasses several types of loans designed for different financial needs and stages of homeownership. Understanding these options is key to leveraging your benefit effectively.

- VA Purchase Loan: This is the most common type, helping eligible individuals buy a new or existing home with competitive interest rates, often with no down payment and no PMI. These loans can be used for single-family homes, condominiums, manufactured homes, and even multi-unit properties (provided the veteran occupies one unit).

- Interest Rate Reduction Refinance Loan (IRRRL), or VA Streamline: If you already have a VA loan, an IRRRL allows you to refinance to a lower interest rate or convert an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. This “VA to VA” loan is designed to be straightforward, often requiring minimal documentation, and in some cases, no new appraisal or income verification. The popularity of IRRRLs saw a significant surge, increasing by 135% in 2025 compared to 2024.

- Cash-Out Refinance: This option allows you to refinance your existing mortgage (VA or conventional) to take cash out of your home equity. This cash can be used for various purposes, such as paying off debt, funding education, or making home improvements. Cash-out refinances also saw a substantial increase, jumping 26.5% year-over-year in 2025.

- Native American Direct Loan (NADL) Program: This unique program helps eligible Native American veterans finance the purchase, construction, or improvement of homes on Federal Trust Land. Unlike other VA loans, the NADL is issued directly by the VA, not a private lender.

- Adapted Housing Grants: While not a loan, these grants assist veterans with certain permanent and total service-connected disabilities in purchasing, constructing, or modifying a home to accommodate their needs.

Loan Limits: A significant update to the VA loan program is the elimination of loan guarantee limits for veterans with full entitlement. This means that if you have full entitlement, the VA will guarantee 25% of your loan amount, regardless of the loan size, allowing you to purchase higher-value homes without a down payment, provided you meet the lender’s financial guidelines. However, if you have partial entitlement, loan limits may still apply. For details on VA loan limits and how they impact your borrowing power, exploring resources on topics like the VA Jumbo Loan can be beneficial.

VA Funding Fee: Nearly all VA loans include a VA funding fee, a one-time charge paid to the VA that helps offset the cost of the program for taxpayers. This fee varies based on your service type, loan amount, and whether it’s your first time using the benefit or a subsequent use. It can typically be financed into the loan amount. However, certain veterans are exempt from paying this fee, most notably those receiving VA disability compensation for a service-connected disability and surviving spouses who are eligible for VA benefits. This exemption further improves the financial advantages of the VA loan for disabled veterans. To understand more about this fee and why VA loans generally don’t have PMI, you can read more about Do VA Loans Have PMI.

Here’s a comparison of some key VA loan types:

| Loan Type | Purpose | Key Features